For thirty years, AI systems have been consumers of money — they cost compute, they cost API calls, they cost human time. Nobody expected them to spend it.

That assumption is breaking. Stripe's update to Link, announced this week, adds explicit support for autonomous AI agents as payment principals. An agent can now hold a wallet, initiate a transaction, and complete a purchase without a human in the loop. This is not a minor API addition. It is the first serious infrastructure signal that AI agents are becoming economic actors.

Here's what the shift means and where it's headed.

Why Agent Commerce Is Different from Bot Payments

The distinction matters. Existing "AI payment" systems are human-initiated with AI assistance — you ask a chatbot to buy something, it fills out a form, you approve. The transaction is human-owned end-to-end.

Agent commerce is different: the agent initiates, the agent decides what to buy, and the agent executes. The human sets budgets and constraints, but the moment of transaction is autonomous. This changes the risk model entirely.

With human-initiated payments:

- Identity is verified at session start (login, MFA)

- Transaction authorization is implicit (you clicked the button)

- Refund and dispute flows assume a human cardholder

- Liability follows familiar consumer protection rules

With agent-initiated payments:

- Identity must be verifiable at the API level, not just at login

- Transaction authorization comes from policy, not a click

- Refund and dispute flows need new handling (who disputes, who gets refunded?)

- Liability is genuinely unclear — who is responsible when an agent spends $400 on the wrong thing?

Stripe's Link update is the first payment infrastructure move toward solving these problems at scale.

What Stripe's Update Actually Does

Stripe Link was already a digital wallet — it stored payment credentials and enabled one-click checkout across sites. The agent update adds two capabilities that matter:

Agent-principal identity: Agents can authenticate as themselves, not as proxies for a human user. This means the agent's identity is tied to its own credential set, separate from any human's account. A travel booking agent and a procurement agent can have different payment profiles, budgets, and spending limits.

Scope-constrained transactions: The agent can't spend beyond what its Link scope allows. A research agent might be authorized for API purchases under $50. A travel agent might be authorized for flights and hotels under $2,000. The payment infrastructure enforces the constraint, not the agent's code.

These two capabilities together make agent commerce auditable, controllable, and reversible in ways that a raw API key to a credit card never would be.

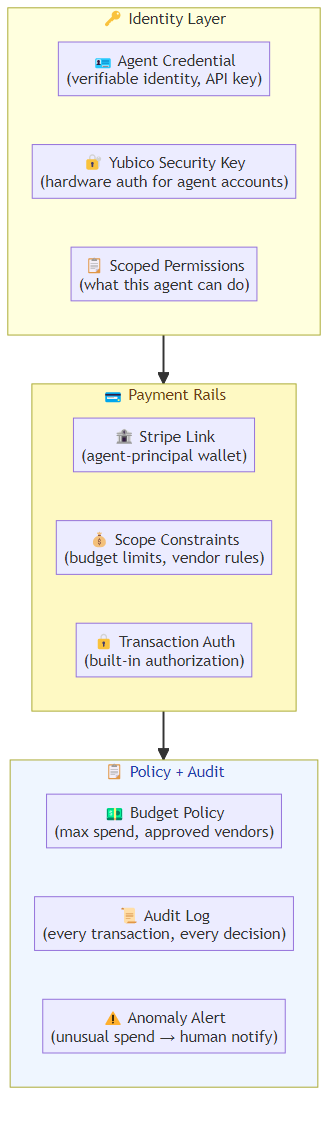

The Agent Commerce Stack Taking Shape

The Stripe update is one layer of a broader infrastructure stack emerging for AI agent commerce:

Identity and authentication: Agents need verifiable identities. This is not just "API keys" — it's credential systems that can express what an agent is authorized to do. Yubico's hardware security keys, now supported by OpenAI for ChatGPT accounts, are part of this layer. Agent identity standards are forming.

Payment rails: Stripe Link, PayPal's agent pay features, and emerging agent-specific payment APIs. These provide the actual transaction infrastructure with built-in authorization constraints.

Budgeting and policy: Above the payment layer, agents need constraint systems that express business logic — not just "you can spend up to X" but "you can only buy from vendors on this approved list" or "this purchase requires a second signature above $500." These constraint systems don't exist yet as standard infrastructure.

Audit and reconciliation: When an agent makes fifty purchases in a day, someone needs to understand what happened. Agent transaction logs, policy violation alerts, and reconciliation workflows are the operational layer that makes agent commerce manageable.

The Stripe update handles the payment rails and partially handles identity. The budgeting, policy, and audit layers are still largely custom work.

Where Agent Commerce Is Real Today

Travel Booking Agents

The clearest early use case. A travel agent that books flights, hotels, and transportation can now complete the transaction end-to-end. The agent has scope constraints (budget, preferred vendors, approval thresholds), initiates the booking, and executes payment. The human reviews the itinerary, not every line item.

Sierra, the enterprise AI startup that just raised $950M, is building customer-facing agents that execute across this stack for B2B customers. Their pitch: the agent doesn't just answer "what flights are available" — it books the flight, sends the confirmation to the traveler's calendar, and files the expense.

Software Procurement

Agents that purchase software subscriptions, API credits, and cloud resources are emerging. An infrastructure agent that detects it's running low on storage can purchase additional capacity from AWS or Snowflake without human intervention. The constraints are tighter here (budget limits, approved vendors) but the use case is compelling.

Research and Data Access

Agents that need to access paid databases, research platforms, or data feeds can now pay for access autonomously. A market research agent that needs a Bloomberg terminal subscription or a specialized dataset can purchase it directly. The payment infrastructure removes the last human bottleneck in the research pipeline.

Content Licensing

With the Academy's new rules excluding AI-generated content from Oscar eligibility and ongoing legal uncertainty around AI training data, agents that license content — images, music, datasets — need to be able to pay for it. This is early and legally complex, but the payment rails are now in place.

The Risk Model Nobody Has Solved

Autonomous spending creates risks that the existing payment ecosystem isn't designed for.

Intent ambiguity: When a human makes a purchase, the intent is clear from the context — you bought the flight because you clicked the button. When an agent makes a purchase, intent must be reconstructed from logs and policy. Was this purchase within the agent's authorized scope? Did it follow the right approval chain?

Failure cascades: An agent that starts spending unexpectedly — either because of a bug or because its constraints weren't strict enough — can execute many transactions before a human notices. Unlike a human who can be alerted mid-action, an agent can complete a burst of transactions faster than human response time.

Dispute and reversal complexity: Chargebacks assume a human cardholder who can explain what went wrong. When an agent makes a purchase, the dispute process needs to reconstruct intent, determine whether the agent followed its constraints, and decide whether the refund goes to the human who authorized the agent or the vendor who delivered the service.

Regulatory uncertainty: Consumer protection laws, financial regulations, and liability frameworks assume human actors. When an agent spends $50,000 on a vendor that turns out to be fraudulent, the liability question is genuinely open — and regulators haven't caught up.

Building Agent Commerce Infrastructure

For teams building agent commerce capabilities:

Start with narrow scope: Don't give agents broad spending authority on day one. Start with low-value purchases (under $50), single vendor relationships, and clear policies. Expand scope as you build confidence.

Build observability before capability: You need transaction logging, anomaly detection, and real-time alerting before you enable autonomous spending. The agent commerce dashboard should show every transaction, its policy justification, and its constraint check results.

Design for human override: Even fully autonomous agents should have pause/cancel capability. If something looks wrong, a human should be able to stop the agent's spending in real time.

Treat the policy layer as product: The constraints that govern agent spending — budget limits, approved vendors, approval thresholds — are part of your product interface. They need to be configurable, auditable, and versioned.

Where Agent Commerce Goes Next

The next eighteen months will see the emergence of agent-first financial products. Not just "agents can use existing payment infrastructure" but "this financial product was designed for agents."

Agent-specific corporate cards with per-agent budgets, transaction limits, and real-time policy enforcement. Insurance products that cover agent-caused losses. Escrow mechanisms for agent-to-agent transactions where both parties need guarantees.

The Stripe update is the opening move. What's coming is a full economic infrastructure for autonomous agents — the banking, accounting, audit, and compliance layer that makes agents credible as economic actors rather than curiosities.

The question for enterprise teams: when your agents can spend money, what constraints do you actually want them to have?

Related posts: AI Agents in the Enterprise: Separating Signal from Hype on ROI — the honest framework for evaluating AI agent business value. Enterprise Agent Deployment — the governance framework for deploying agents that handle real transactions. Physical AI Agents — the next frontier where AI agents operate in the physical world.