The product competition in AI is no longer about text.

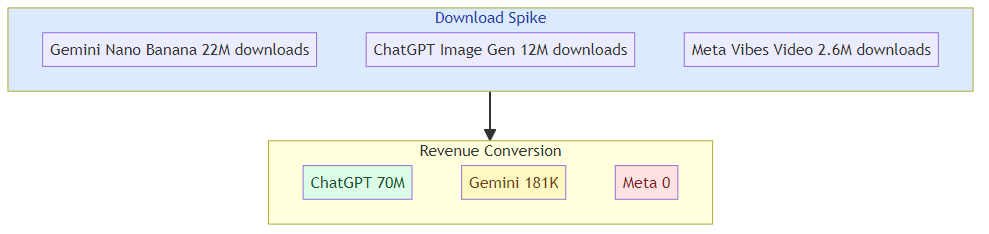

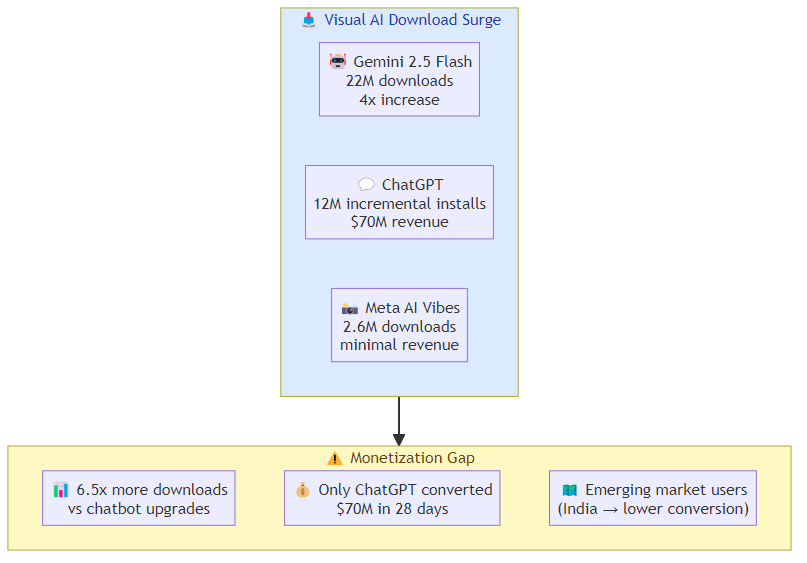

According to Appfigures data, image AI model releases are driving 6.5x more app downloads than equivalent chatbot feature upgrades. GPT-4o's image model launch added 12 million incremental installs to ChatGPT. Google's Gemini 2.5 Flash image model (the "Nano Banana" release) drove 22 million additional downloads in 28 days — a 4x increase. Meta AI's visual features added 2.6 million downloads.

But here's the number that matters: ChatGPT was the only platform that converted the image AI download surge into meaningful revenue — $70 million in gross consumer spending over 28 days. Gemini and Meta AI saw minimal or no revenue impact despite download numbers that would make any product team jealous.

The visual AI arms race is real, and it's changing how AI companies think about product strategy. But the monetization gap is also real, and it's forcing a reckoning with the difference between attention and business model.

Why Visual AI Wins on Downloads

The download differential has a straightforward explanation: visual outputs are more shareable than text outputs.

A user who generates an image with AI has something to post. A user who gets a good text response has... a text response. The shareability of AI-generated images creates a viral loop that pure text AI cannot replicate. Every social media post with an AI-generated image is an advertisement for the tool that created it.

This creates a download incentive that is structurally different from chatbot improvements. A better chatbot is valuable to existing users but doesn't generate external visibility. A surprising, impressive, or funny AI image propagates on its own — and brings new users with it.

The product implication: visual AI features have a lower customer acquisition cost than text AI features, purely because of the viral coefficient built into shareable images.

The Monetization Gap

The revenue picture reveals the other side of the coin. ChatGPT generated $70M in consumer spending from its image model in 28 days. Gemini generated the same order of magnitude in downloads but effectively no revenue.

Why? Three structural factors:

Different user populations: Gemini's image model surge was disproportionately driven by emerging markets (India specifically, based on Appfigures data) where paid subscription conversion rates are structurally lower. The download volume doesn't match the paying-user demographic that drives revenue.

Different product integration: ChatGPT's image generation is tightly integrated into an existing subscription product where users already have payment instruments on file. Gemini's image feature is more of a standalone novelty that doesn't push users toward paid tiers as effectively.

Different monetization infrastructure: ChatGPT had the subscription model in place. Gemini is still finding its monetization architecture for consumer AI products.

The pattern suggests that visual AI download surges are a necessary but not sufficient condition for revenue growth. The monetization infrastructure — subscription tiers, payment integration, upgrade prompts, and the right user demographic — determines whether downloads convert.

What This Means for AI Product Strategy

The product lessons from the image AI download surge are relevant for any AI company building consumer or enterprise products:

Visual features as acquisition, not monetization: treating visual AI capabilities as top-of-funnel acquisition tools rather than revenue generators changes how you evaluate their ROI. Gemini's 22M downloads are valuable even without immediate revenue — they're brand awareness, user education, and competitive positioning.

Shareability as a design principle: AI features that produce shareable outputs have a different growth profile than features that don't. When designing AI products, the question "does this produce something a user would share?" should be part of the feature evaluation, not an afterthought.

The conversion gap as a product challenge: the monetization conversion gap between ChatGPT and Gemini suggests that the product integration matters as much as the AI capability. ChatGPT's image model is a feature of a product people pay for. Gemini's image model is closer to a standalone demo. The product context determines monetization potential.

The Enterprise Angle

Visual AI capabilities also matter in enterprise contexts in ways that pure text AI doesn't. Consider:

Manufacturing and design: AI image generation for product prototyping, interior design visualization, and architectural rendering is finding strong enterprise adoption where the output has direct business value.

Marketing and content: Enterprise marketing teams use visual AI for campaign imagery, social content, and presentation materials. The ROI calculation is clearer when the image replaces a expensive photoshoot rather than just being an impressive demo.

Documentation and training: visual AI for diagram generation, flowchart creation, and training material illustration has enterprise use cases that are emerging but not yet fully exploited.

The enterprise visual AI market is less about the viral download dynamic and more about the integration into workflows where visual output has concrete business value. The monetization path in enterprise is different from consumer: it's about efficiency gains and cost reduction rather than subscription conversion.

The Competitive Dynamics

The visual AI race is now multi-platform: OpenAI (GPT-4o), Google (Gemini 2.5 Flash), Meta AI, and emerging players all competing for the same visual AI use cases. The competitive pressure is pushing model quality up rapidly — image generation quality that was state-of-the-art six months ago is now commodity.

For product teams: the differentiation is moving from model quality (which commoditizes) to product integration and workflow embedding. The company that figures out how to make visual AI fit naturally into existing workflows will capture more value than the company that builds the technically best image generator.

For users: the quality of visual AI is reaching a threshold where the limiting factor is not "can the model generate this image?" but "what should I ask it to generate?" The productivity question in visual AI is shifting from generation quality to generation direction — which is a more interesting and harder problem.

Related posts: AI Chip Infrastructure — how the infrastructure layer enables AI product capabilities. AI Agents in Production — building AI products that are more than demos.