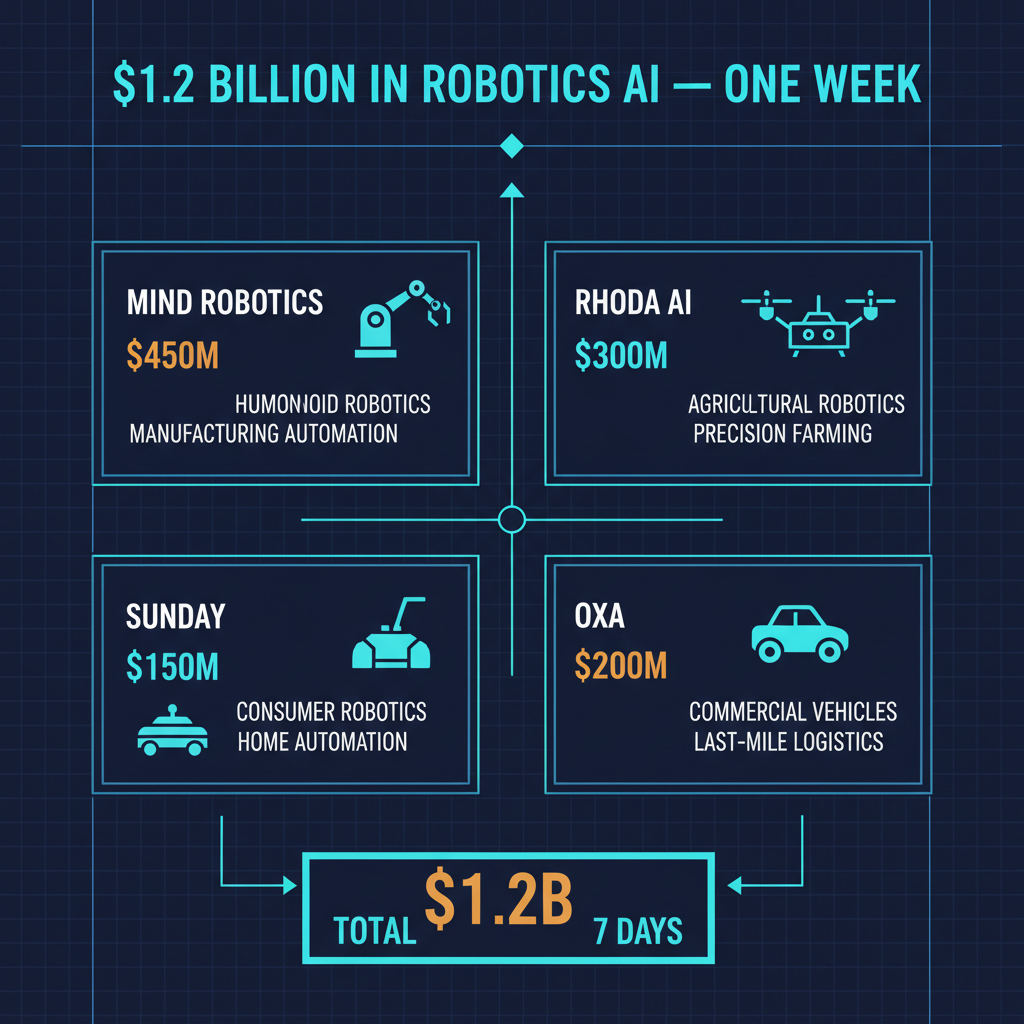

In the second week of March 2026, something happened in AI venture capital that deserves more attention than it received. Four robotics companies raised a combined $1.2 billion in funding. Mind Robotics closed a $500 million round. Rhoda AI secured $450 million. Sunday achieved unicorn status with a $165 million raise. Oxa brought in $103 million. Separately, Nexthop AI raised $500 million for AI-powered networking infrastructure. These are not small rounds for speculative technologies. These are serious capital commitments into the physical embodiment of artificial intelligence.

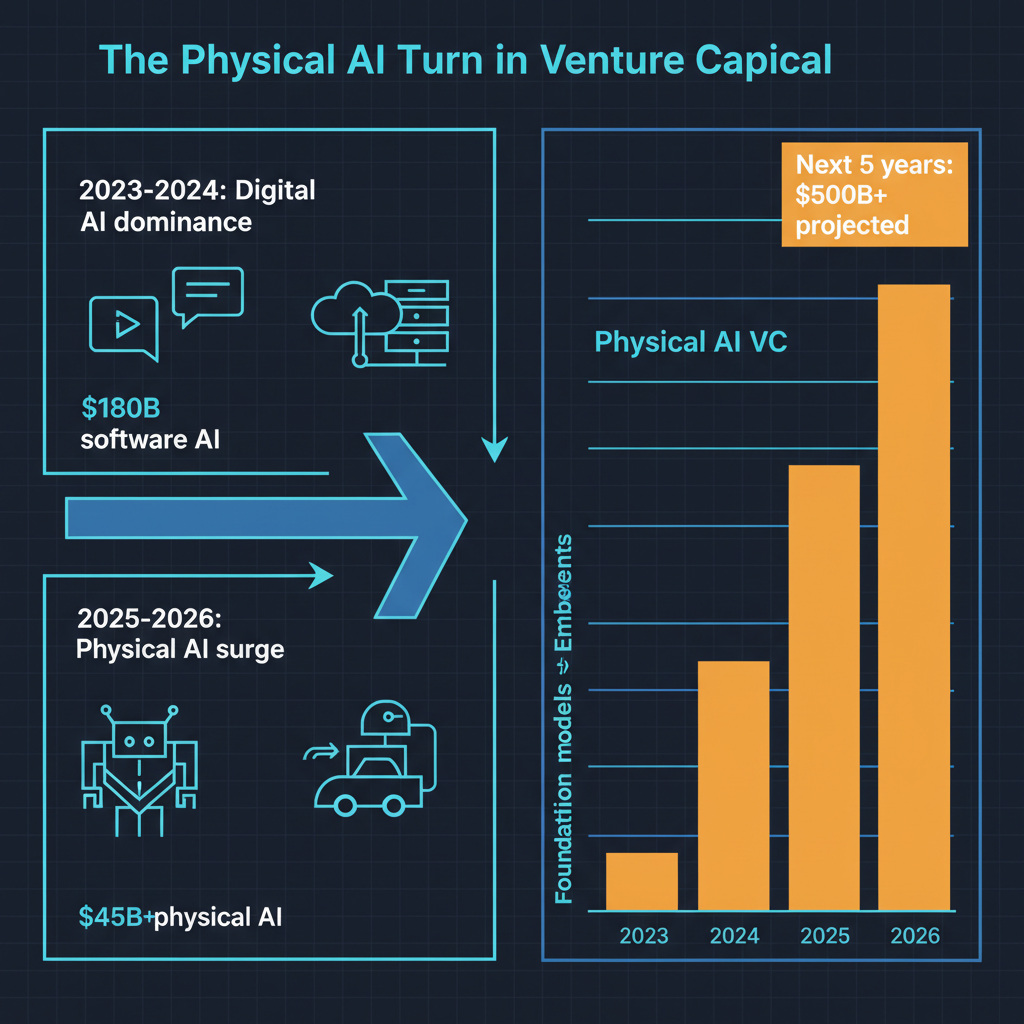

I have been following the AI funding landscape closely for several years, and this week marks a turning point. The center of gravity in AI investment is shifting from software that generates text and images to machines that interact with the physical world. This is the beginning of what I think will be the dominant AI narrative of the next five years: the move from digital intelligence to physical intelligence.

The Four Companies and What They Represent

Each of the four robotics companies that raised capital represents a different slice of the physical AI opportunity, and together they map out the full territory.

Mind Robotics, with its $500 million round, is focused on industrial automation. Their approach combines large language model reasoning with robotic manipulation, aiming to create systems that can understand natural language instructions and translate them into physical actions on factory floors. This is not the narrow, pre-programmed industrial robotics that has existed for decades. This is adaptive automation that can handle variability, understand context, and adjust to changing conditions in real time.

Rhoda AI's $450 million raise targets the household and personal assistance market. Their robots are designed to operate in unstructured home environments, which is arguably the hardest robotics problem there is. A factory floor can be controlled and standardized. A kitchen in a family home cannot. The robot must navigate unpredictable layouts, handle fragile objects, understand social context, and operate safely around children and pets. Solving this problem at scale would be transformative for elder care, disability assistance, and household labor.

Sunday, which crossed the unicorn threshold with its $165 million round, is building autonomous logistics systems. The company focuses on last-mile delivery and warehouse operations, two areas where labor costs are high, margins are thin, and the business case for automation is immediately compelling. Their robots operate in semi-structured environments, which is a sweet spot that is more tractable than household robotics but more complex than factory settings.

Oxa's $103 million round funds their autonomous vehicle and mobile robotics platform. Rather than building a fully autonomous consumer car, Oxa has focused on defined operational domains: industrial sites, logistics hubs, and specific urban corridors where the operating conditions can be bounded and validated.

Why Now? The Convergence That Makes This Possible

Physical AI has been "five years away" for roughly thirty years. What has changed to make investors commit $1.2 billion in a single week?

Three technical convergences have shifted the feasibility equation. The first is foundation models for robotics. Just as large language models transformed natural language processing by providing a general-purpose foundation that could be fine-tuned for specific tasks, researchers have begun developing foundation models for robotic control. These models, trained on vast datasets of simulated and real-world manipulation tasks, give robots a general understanding of physics, spatial reasoning, and object interaction that dramatically reduces the engineering required for each new task.

The second convergence is simulation-to-reality transfer. Training robots in the physical world is slow, expensive, and dangerous. The breakthroughs in physics simulation, particularly GPU-accelerated simulators like NVIDIA Isaac Sim, have made it possible to train robotic systems on millions of scenarios in simulation and transfer that learning to physical hardware with reasonable fidelity. This changes the economics of robotics development from hardware-constrained to compute-constrained, and compute is something we know how to scale.

The third convergence is hardware cost reduction. Actuators, sensors, and compute modules have all dropped in cost while improving in capability. A robotic manipulation system that would have cost $250,000 five years ago can now be built for under $50,000, with significantly better perception and control. This brings robotics from the domain of large manufacturers with capital budgets to small and medium enterprises.

The Nexthop AI Factor

Nexthop AI's $500 million raise for AI-powered networking infrastructure is not a robotics investment, but it is deeply connected to the physical AI thesis. As robots proliferate in warehouses, factories, and homes, the networking infrastructure that connects them, coordinates their actions, and processes their sensor data becomes a critical bottleneck. Nexthop is building intelligent networking systems that can dynamically allocate bandwidth, prioritize safety-critical communications, and handle the latency requirements of real-time robotic control. This is the plumbing that physical AI requires, and the size of the round reflects the scale of the opportunity.

Physical AI vs. Digital AI: A Different Investment Thesis

Investing in physical AI is fundamentally different from investing in software AI, and investors who do not understand this distinction will get burned.

Software AI companies can iterate rapidly, deploy globally with minimal marginal cost, and scale without physical infrastructure. A new version of ChatGPT reaches hundreds of millions of users instantly. Physical AI companies must deal with manufacturing, supply chains, regulatory approvals, physical deployment, maintenance, and the stubborn reality that atoms are harder to move than bits.

But the flip side is that physical AI companies, once deployed, have much deeper moats than software AI companies. A factory that has reconfigured its entire production line around a particular robotics platform does not switch vendors easily. A logistics company that has built its warehouse operations around autonomous mobile robots has real switching costs. The workflow integration that creates defensibility in software AI is even more pronounced in physical AI, where the integration is literally built into the physical infrastructure.

The total addressable market for physical AI is also staggering. Global logistics is a $10 trillion market. Manufacturing is $16 trillion. Household services are $600 billion. Even modest penetration of these markets by autonomous systems represents revenue opportunity that dwarfs the current AI software market.

What I Am Watching

Several things will determine whether this week's $1.2 billion in robotics funding represents the beginning of a durable trend or a venture capital enthusiasm that will not survive contact with physical reality.

Safety and regulatory frameworks. Autonomous robots operating in shared human spaces need clear safety standards and regulatory approval processes. The EU is ahead of the United States on this front with its Machinery Regulation update, but the regulatory landscape is still immature. Companies that invest in safety certification early will have advantages; companies that cut corners will set the industry back.

The simulation-to-reality gap. Despite enormous progress, transferring learned behavior from simulation to the physical world remains imperfect. Edge cases that never appear in simulation appear constantly in real deployments. The companies that solve the long tail of real-world variability will win; those that demo well in controlled settings but fail in deployment will not.

Labor market dynamics. Physical AI adoption will be shaped by labor economics as much as by technology. In markets with severe labor shortages, like Japan's aging population or the chronic shortage of warehouse workers in the United States, the adoption case is immediate. In markets with abundant labor, the economics are less compelling and the social resistance is greater.

The integration challenge. The most underrated challenge in physical AI is not the robot itself but integrating it into existing workflows, systems, and human teams. The companies that think carefully about human-robot collaboration, rather than full human replacement, will find faster adoption paths and less resistance.

The Bigger Picture

We are at the beginning of a transition from AI as software to AI as a physical presence in the world. The $1.2 billion raised in one week is a signal, not an anomaly. The technical foundations are in place. The capital is being deployed. The market need is real.

But I want to temper the enthusiasm with a note of historical perspective. The first wave of autonomous vehicle investment, from roughly 2016 to 2022, saw tens of billions of dollars deployed with results that fell far short of the initial promises. Physical AI will face similar challenges: hardware is unforgiving, safety requirements are non-negotiable, and the gap between demo and deployment is vast.

The difference this time is that the underlying AI capabilities are genuinely more mature, the hardware is genuinely cheaper and better, and the investment is spread across multiple practical applications rather than concentrated in the single hardest problem in robotics, which is full self-driving on public roads. This portfolio approach to physical AI gives the thesis a better chance of producing real returns, even if individual companies struggle.

The age of embodied intelligence is arriving. It will be messier, slower, and more complicated than the digital AI revolution. It will also be more consequential.