February 2026 will be remembered as the month that rewrote the rules of startup finance. Global startup funding hit $189 billion in a single month — a record that would have seemed absurd even twelve months ago. The engine behind this number is AI, and specifically the convergence of enormous revenue growth at frontier AI companies, a new class of sovereign and strategic investors entering the market, and an application layer that is finally generating enterprise-grade returns.

Two and a half weeks into March, we have already seen more $100 million-plus AI funding rounds than in any comparable period in venture capital history. The capital is not trickling into AI. It is flooding in.

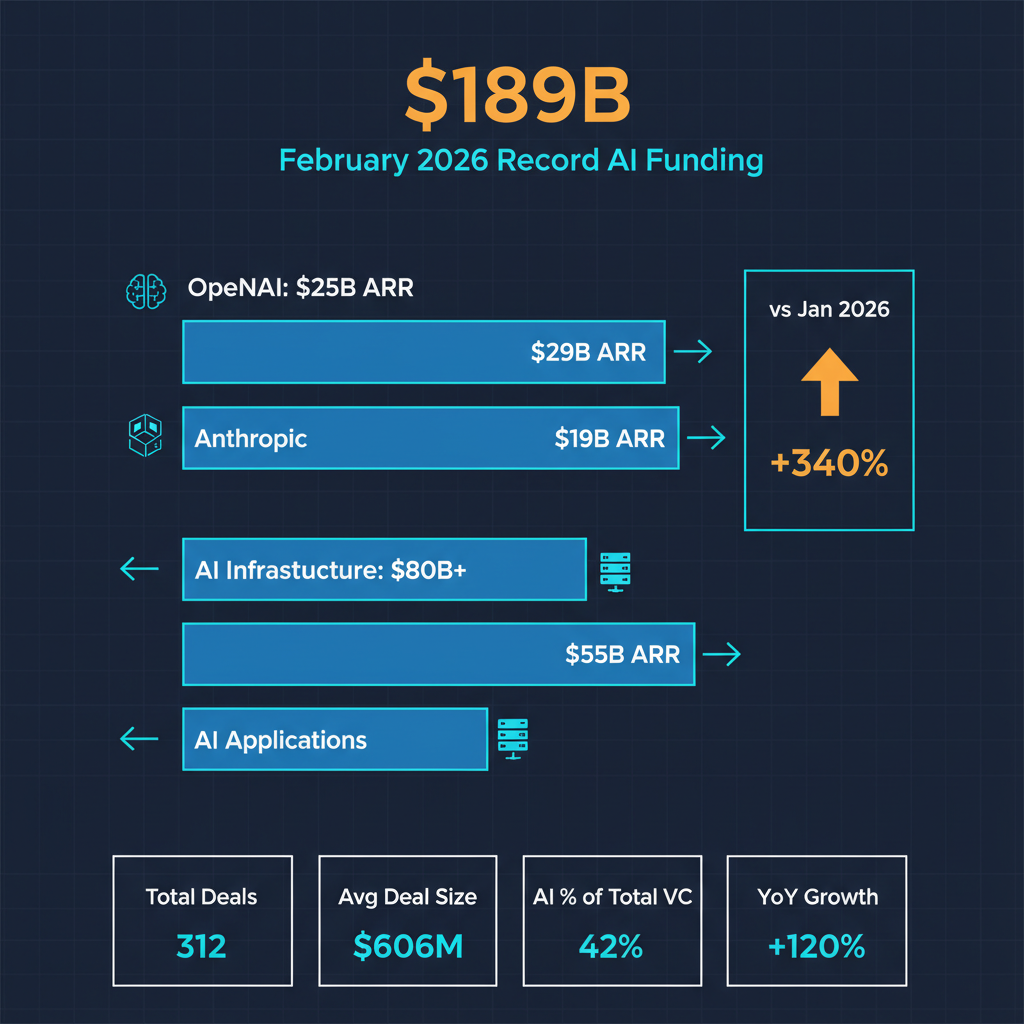

The Numbers Behind the Record

The headline figure of $189 billion in February deserves decomposition. This was not a single mega-round distorting the data. It was broad-based, with AI deals accounting for the majority of total venture deployment across every major geography. The United States led by volume, but Europe and the Middle East posted their largest monthly AI investment totals as well.

At the company level, the revenue trajectories justify at least some of the enthusiasm. OpenAI has surpassed $25 billion in annualized revenue, a figure that puts it in the same revenue class as companies like Salesforce — except OpenAI reached this level in a fraction of the time. Anthropic is approaching $19 billion annualized, with enterprise contract growth that has been consistently accelerating quarter over quarter. These are not projections or TAM slides. These are real revenue numbers from real customers paying real money for AI capability.

The infrastructure layer is seeing comparable capital concentration. CoreWeave, which provides GPU cloud infrastructure purpose-built for AI workloads, has raised billions in debt and equity. NVIDIA's market capitalization continues to reflect the fact that it is the essential supplier for an industry spending tens of billions on compute.

Why This Time Feels Different

I have watched enough technology hype cycles to be instinctively skeptical of "this time is different" narratives. But there are structural differences between the current AI investment wave and previous technology bubbles that are worth understanding.

The dot-com bubble was built on revenue projections. Companies raised enormous sums on business plans that assumed internet adoption curves that had not yet materialized. The crypto boom of 2021 was built on speculative asset appreciation with minimal underlying utility for most participants. The AI funding wave of 2026 is built on actual revenue at scale. When OpenAI generates $25 billion in annualized revenue, and enterprise customers are signing multi-year contracts, the investment thesis is grounded in observable commercial traction, not speculative adoption curves.

The second structural difference is the breadth of the buyer base. AI products are being purchased by law firms, hospitals, manufacturing companies, financial institutions, government agencies, and individual consumers. This is not a technology being adopted by a narrow early-adopter segment. It is broad-based enterprise and consumer adoption happening simultaneously, which is rare in technology history.

The third difference is the capital efficiency of AI application companies. Unlike the infrastructure layer, which requires billions in GPU investment, AI application startups can build on top of foundation model APIs with relatively modest capital requirements. A company like Cursor reached unicorn status with a fraction of the capital that traditional enterprise software companies required. This means the return on invested capital for successful AI application startups can be extraordinary.

The Case for Caution

All of that said, I think there are real reasons for concern about the current pace of capital deployment.

The most obvious risk is valuation compression. Several AI companies have raised at revenue multiples that assume continued hypergrowth for years. OpenAI's valuation implies a forward revenue trajectory that requires it to become one of the largest software companies in history. Anthropic's valuation makes similar assumptions. These outcomes are possible, but they are not guaranteed, and the number of AI companies that can simultaneously achieve these growth trajectories in the same market is limited by the total addressable demand.

The second risk is the infrastructure overshoot. The amount of capital being deployed into GPU clusters, AI-optimized data centers, and inference infrastructure assumes a demand curve that may not materialize at the projected pace. If enterprise AI adoption plateaus or grows more slowly than projections suggest — due to integration challenges, regulatory friction, or simply the difficulty of changing enterprise workflows — the infrastructure buildout will have outpaced demand, creating stranded capital.

The third risk is the competitive dynamics at the application layer. There are currently dozens of well-funded AI startups in every major vertical — legal AI, healthcare AI, financial AI, sales AI. The market cannot support all of them. Consolidation is inevitable, and the companies that raised at peak valuations will face the most painful adjustments. This is not a systemic risk — it is normal market dynamics — but it will be painful for the specific companies and investors caught in the correction.

What the Smart Money Is Actually Doing

The most instructive signal in the current market is not the total dollar volume — it is where the most sophisticated investors are concentrating their bets.

Sovereign wealth funds from the Middle East and Southeast Asia have become major AI investors, bringing patient capital and strategic alignment to companies building infrastructure. This is different from traditional venture capital in both time horizon and motivation. These investors are not looking for quick returns — they are positioning their national economies for an AI-driven future.

Corporate strategic investors — NVIDIA, Microsoft, Google, Amazon, Samsung — are investing to secure their positions in the AI supply chain. NVIDIA's investment in AI startups is not primarily a financial bet; it is a strategy to ensure that the most important AI companies are built on NVIDIA hardware and remain loyal customers.

The traditional venture firms, meanwhile, are increasingly differentiating between the infrastructure layer (where they are deploying larger checks into fewer companies) and the application layer (where they are making more bets with smaller checks, expecting high failure rates but outsized returns from winners).

My Assessment

I do not think the current AI investment cycle is a bubble in the dot-com sense. The underlying technology works, the revenue is real, and the enterprise adoption is genuine. But I do think the current pace of capital deployment has outrun the pace at which the market can absorb and productively deploy that capital.

The most likely outcome is not a dramatic crash but a gradual repricing. Some companies that raised at 200x revenue multiples will need to grow into their valuations over longer timeframes than their investors anticipated. Some infrastructure bets will take longer to generate returns than projected. Some application-layer startups will discover that their moats are thinner than they believed when the underlying models improve and their differentiation narrows.

The companies that will thrive through this repricing are the ones with genuine revenue growth, real competitive moats, and capital discipline. OpenAI and Anthropic are generating revenue at a pace that can justify extraordinary valuations. The infrastructure companies with long-term contracts and genuine capacity constraints will be fine. The application companies with deep workflow integration and proprietary data flywheels will compound.

The $189 billion February is a milestone that marks the AI industry's transition from an emerging technology sector to a major force in the global economy. The capital is real. The technology is real. The question that remains is whether every individual bet within this wave is as well-grounded as the aggregate trend suggests. History says it will not be. But the aggregate trend — AI as the defining technology platform of this decade — is as strong as any I have seen in my career.